Finanzinstitute sind nach § 24c Abs. 1 KWG verpflichtet, einen Datenpool zu führen, in dem festgelegte Kunden- und Kontostammdaten (z.B. Kontonummer, Name und Geburtsdatum der Kontoinhaber und Verfügungsberechtigten, Eröffnungs- und Schließungsdatum) gespeichert sind.

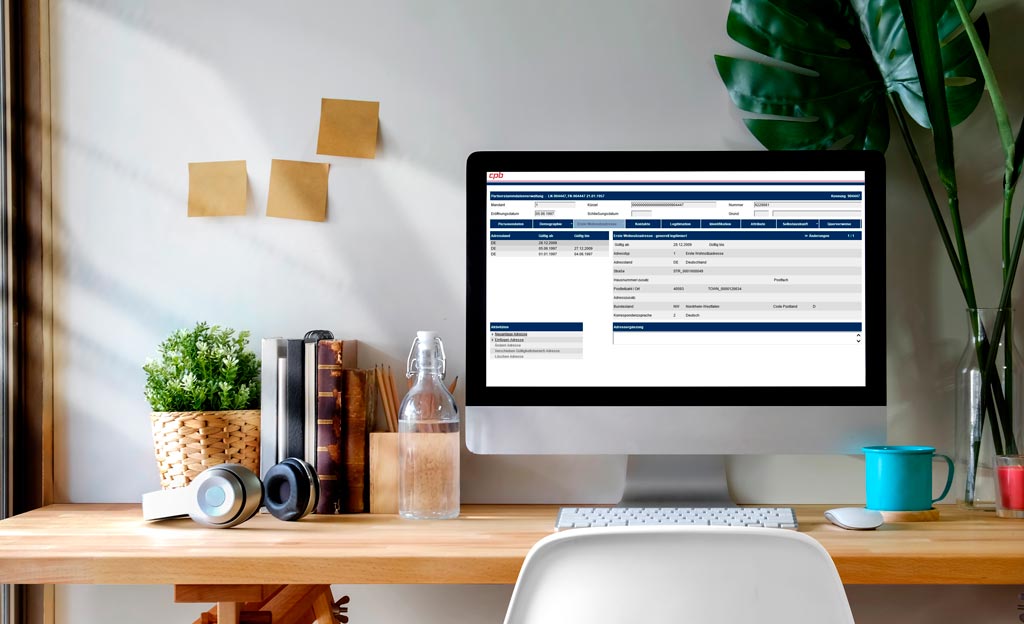

In SECTRAS steht eine Komponente zur Verfügung, die die relevanten Daten aus den zentralen Stammdatensystemen entsprechend der gesetzlichen Vorgaben aufbereitet und an die Kontoevidenzzentrale des Bank-Verlag weiterleitet.

CPB übernimmt das Hosting, die vollständige Umsetzung (Konvertierung) in das vorgeschriebene Meldeformat, die gesetzliche Aufbewahrung und die Kommunikation mit der Kontenevidenzzentrale.